Retail medicine pricing and availability project

Project background

High levels of out-of-pocket spending on life-saving medicines underscore the need for better visibility into the prices consumers pay outside of public-sector channels. Yet retail medicine pricing data is often fragmented, inaccessible, or unavailable. Policymakers, manufacturers, distributors, and clients were unaware of the patterns showing how patients find medicines, what they have to pay, and where retail supply is breaking down.

In response, Project Last Mile (PLM) was commissioned by the Gates Foundation to design a low-cost approach to monitoring retail medicine prices and availability. The approach drew on proven methods used by Fast Moving Consumer Goods (FMCG) corporations, adapted to the practical realities of healthcare access in Africa, and was intended to generate evidence to support future scale-up.

Approach

Driven by consultations with the Gates Foundation, PLM developed a priority medicine list covering malaria, maternal, newborn and child health, family planning, hypertension, diabetes, HIV, and tuberculosis. The list was then expanded to reflect the range of formulations, strengths, pack sizes, and brands available in the market. A data-collection tool was developed, enumerators were trained, and fieldwork was undertaken, followed by data cleaning and validation.

Kenya was selected as the pilot market, and lessons from that initial implementation were used to strengthen subsequent surveys in Nigeria, Ethiopia, the Democratic Republic of the Congo, and Mozambique. Additional insights from these markets can, in turn, be incorporated into future survey rounds to further improve efficiency, consistency, and relevance.

In total, approximately, 4,900 data points were collected from 537 retail pharmacies.

In addition to medicine price and availability data, the exercise captured information on suppliers, delivery frequency, and stockouts. The principal deliverables for the Gates Foundation were the full dataset and a detailed description of the methodology.

Analysis of data revealed multiple areas of concern

Affordability challenges

Example: hydrochlorothiazide (hypertension)

- 193 data points collected in one country

- This chronic medication has 85% of data for singles for a daily dosage tablet

Stockouts

- Stockouts reported to varying degrees

- Ethiopia and Mozambique outlets appeared less impacted than others

- Separate questions on delivery frequency and wholesalers could also give pointers to the root causes

- Positive feedback that for all categories, stockouts appear to be improving

Lack of price ladders for consumers to see value in buying a full prescription

Example: iron and folic acid

- In many cases, the single offered better value versus larger pack sizes

- Examples used are from Kenya and Nigeria, where most data points were captured

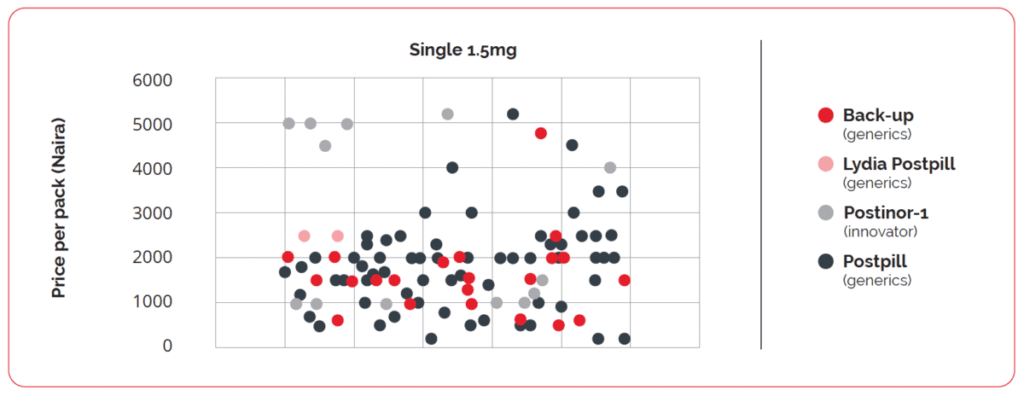

Uneven or lack of price gaps between innovator and generics

Example: emergency contraceptive pill

- Generics should be significantly lower

- In this example, the innovator and generics are found at similar prices

We believe the data can be used to drive access, with the following recommended pathway:

The data exists — and is actionable

Five countries. 4,924 data points. 527 outlets. This study presents a comprehensive cross-country dataset on retail medicine pricing in sub-Saharan Africa. The affordability index, price ladder gaps, and stockout patterns identified here are specific, quantifiable, and ready for action.

FMCG frameworks apply directly

Coca-Cola’s Opening Price Point, Unilever’s Affordability Index, P&G’s price ladder principles, and Nestlé’s rural pricing model all translate directly into medicine access strategy. The gap between FMCG practice and medicine pricing is a choice, not a structural barrier.

The value chain must be engaged, not just the consumer

Price improvements at the pharmacy counter require manufacturers, importers, wholesalers, and pharmacists to all see a “win.” Incentive schemes that align commercial interests with access outcomes are the levers that make change stick.

Other developing countries have shown the way

India, Brazil, Indonesia, and Bangladesh have all achieved 30–85% generic medicine penetration through combinations of prescribing mandates, reference pricing, pharmacist substitution rights, and retailer incentives. None required a systemic overhaul, but all relied on targeted interventions at scale.

Stockouts are as important as price

A medicine that is available but unaffordable and one that is affordable but out of stock produce the same outcome for the patient: no access. Supply chain interventions — fortnightly delivery for chronic medicines, wholesaler transparency, and cold chain investment — must run in parallel with pricing work.

PLM could be a unique partner to catalyze this

PLM’s track record of adapting the Coca-Cola system expertise to health supply chains, combined with the now-available unique dataset, positions it to convene the value chain, design the incentive scheme, and provide the independent monitoring function that all actors need.

Key findings

The analysis highlighted several important patterns with implications for access to medicine, affordability and market functioning in the private retail sector.

- Affordability constraints were driving retailers to sell chronic medicines often purchased in single units or weekly packs rather than in full prescription quantities.

- Pricing structures for larger pack sizes did not appear to consistently incentivize consumers to purchase a full course of treatment.

- While it would be reasonable to assume that generics would be cheaper than innovator brands for the same formulation, pricing differences between innovator and generic products varied, indicating system-wide pricing inefficiency.

- Stockouts were reported across all medicine categories in the sample, although retailers indicated that availability had improved compared with the previous year.

- The initial list of 31 medicines expanded to approximately 200 distinct SKUs across formulations, strengths, and pack sizes. However, an average of only 9 SKUs was recorded per outlet, indicating limited availability or weak demand. Of the 31 medicines, 16 were identified as having very low coverage, particularly HIV and tuberculosis products, where the public health sector continued to meet a significant share of patient need.

Conclusion and next steps

The project demonstrated that private-sector retail pharmacy data on medicine prices, availability, and stockouts can be collected in a relatively short period and across a wide range of brands, formulations, strengths, and pack sizes. It also showed that both country-specific and cross-cutting lessons can be applied to make future data-collection exercises simpler, faster, and potentially more cost-effective.

The resulting data has practical relevance for a wide range of stakeholders, including global health initiative funders, Ministries of Health, and private-sector actors across the medicine value chain. It provides an evidence base to inform more targeted interventions to improve access to medicine in underserved markets.

The next step is to translate these insights into focused initiatives that address the most important access barriers identified in the analysis. Drawing selectively on fast-moving consumer goods principles relevant to the health sector, PLM can help design programs that engage actors across the value chain, including retailers, wholesalers, importers, and manufacturers.

A test-and-learn approach, focused on selected products and markets with willing participants, is recommended as a practical way to build evidence, refine interventions, and identify scalable models over time.

Access the dataset

The full dataset and methodology are available on request.

If you are interested in accessing the dataset or learning more about the project, please contact us.